“I don’t subscribe to labels. Unless I’m labelling other people” *

I met a US Equity fund manager in Dublin last week who told me about a “once in a lifetime” opportunity for his style of investing. In fairness to him, he did say that he had been through town almost exactly 12 months ago and said exactly the same thing!

He was a Value fund manager. And a very good one. His fund has a very good performance track record against other value managers.

I’m not so sure I get all this label stuff – like Value or Growth. Certainly I think it sounds better to be a value investor, and that value matters. It wouldn’t seem right to set out to buy things that weren’t good value. Value also sounds right and a bit homely. Value in the world of investments means you’re looking for stocks that trade at a price, where that price relative to its book value or relative to earnings is less than the average in the market. The more conservative you are, the more of a discount against the average you might look for. And if you want to be really sneaky you’ll use words like “intrinsic value” which is basically whatever you’re having yourself.

And then there’s Growth. Here you’re buying stocks where you think the growth in earnings or sales is going to be better than the average. (For shorthand think Amazon or Google). Equally growth sounds nice too!

The idea is that when times are bad and growth is scarce or in short supply, investors should place a premium on stocks that can deliver growth. On the other side when things are picking up, value stocks are the best and cheapest way of getting a slice of the action.

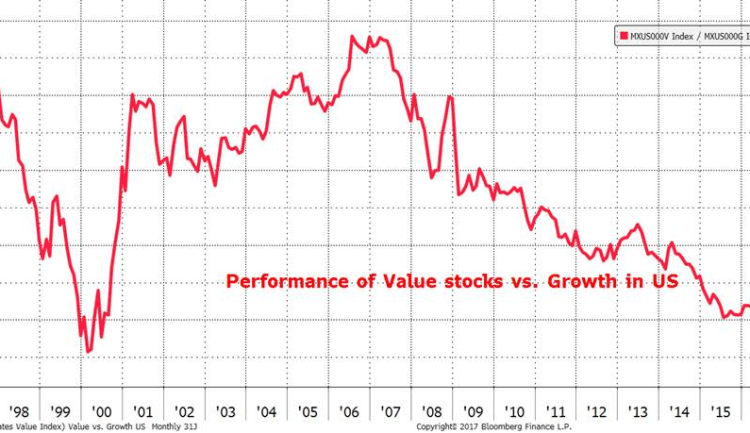

Now the investing world is divided into those who swear by Value as a strategy to make money and those who swear by Growth. And the Value folks will point out how if you go back 30/40 years owning a “Value” portfolio has made you better off than owning a “Growth” one. Problem is since 2007 Value has performed poorly compared to Growth – and that’s about 10 years. (I’ve had careers shorter than that). That’s why I’m not too keen on labels. The length of time when your label can be out of favour can be very long indeed. (See graph)

And I know that the discount between value stocks and the market overall is as wide as it’s ever been and yes we did see a bit of a bounce in Value in last quarter of 2016 into this year, but I’m not sure I know what the catalyst is for a sustained period of out-performance. They used to say rising bond yields were well correlated with the value style performing but I suspect that’s because they were seen as a proxy for better growth. Economic growth today is good and looks resilient but “Value” is not responding. John Authers in The Financial Times thinks this means investors are generally negative.

I wouldn’t hang my investment hat on either style, given how long they can be out of favour and that it’s difficult to call the turning points. Also I think stocks which in the past were considered value, may now have valuations which shoves them into a growth basket.

I’d rather look for stocks which are mispriced relative to their potential, whether that’s driven by assets or future profits.

I do think these labels may play a role in risk management in as much as high flying growth stocks when they do hit an air pocket in terms of some disappointment can fall sharply whereas expectation in the value sector may be more modest to begin with.

*Gaby Dunn